by David Stockman

There has never been a more destructive central banking policy than the Fed’s current maniacal quest to stimulate more inflation and more debt. That’s what is killing real wages and economic vitality in flyover America—-even as it showers prodigious windfalls of unearned wealth on Wall Street and the bicoastal elites who draft on the nation’s vastly inflated finances.

In fact, the combination of pumping-up inflation toward 2% and hammering-down interest rates to the so-called zero bound is economically lethal. The former destroys the purchasing power of main street wages while the latter strip mines capital from business and channels it into Wall Street financial engineering and the inflation of stock prices.

In the case of the 2% inflation target, even if it was good for the general economy, which it most assuredly is not, it’s a horrible curse on flyover America. That’s because its nominal pay levels are set on the margin by labor costs in the export factories of China and the EM and the service sector outsourcing shops in India and its imitators.

Accordingly, wage earners actually need zero or even negative CPI’s to maximize the value of pay envelopes constrained by global competition. Indeed, in a world where the global labor market is deflating wage levels, the last thing main street needs is a central bank fanatically seeking to pump up the cost of living.

So why do the geniuses domiciled in the Eccles Building not see something that obvious?

The short answer is they are trapped in a 50-year old intellectual time warp that presumes that the US economy is more or less a closed system. Call it the Keynesian bathtub theory of macroeconomics and you have succinctly described the primitive architecture of the thing.

According to this fossilized worldview, monetary policy must drive interest rates ever lower in order to elicit more borrowing and aggregate spending. And then authorities must rinse and repeat this monetary “stimulus” until the bathtub of “potential GDP” is filled up to the brim.

Moreover, as the economy moves close to the economic bathtub’s brim or full employment GDP, labor allegedly becomes scarcer, thereby causing employers to bid up wage rates. Indeed, at full employment and 2% inflation wages will purportedly rise much faster than consumer prices, permitting real wage rates to rise and living standards to increase.

Except it doesn’t remotely work that way because the US economy is blessed with a decent measure of free trade in goods and services and virtually no restrictions on the flow of capital and short-term financial assets. That is, the Fed can’t fill up the economic bathtub with aggregate demand because it functions in a radically open system where incremental demand is as likely to be satisfied by off-shore goods and services as by domestic production.

This leakage through the bathtub’s side portals into the global economy, in turn, means that the Fed’s 2% inflation and full employment quest can’t cause domestic wage rates to rev-up, either. Incremental demands for labor hours, on the margin, are as likely to be met from the rice paddies of China as the purportedly diminishing cue of idle domestic workers.

Indeed, there has never been a theory so wrong-headed. And yet the financial commentariat, which embraces the Fed’s misbegotten bathtub economics model hook, line and sinker, disdains Donald Trump because his economic ideas are allegedly so primitive!

The irony of the matter is especially ripe. Even as the Fed leans harder into its misbegotten inflation campaign it is drastically mis-measuring its target, meaning that flyover American is getting an extra dose of punishment.

On the one hand, real inflation where main street households live has been clocking in at over 3% for most of this century. At the same time, the Fed’s faulty measuring stick has registered a persistent inflation shortfall.

So in order to combat this phony run of “insufficient” inflation, our monetary central planners have kept interest pinned to the zero bound for 89 straight months, thereby fueling the gambling spree in the Wall Street casino. The baleful consequence is that more and more capital has been diverted to financial engineering rather than equipping main street workers with productive capital equipment.

As we indicated in Part 1, even the Fed’s preferred inflation measuring stick——the PCE deflator less food and energy—has risen at a 1.7% rate for the last 16 years and 1.5% during the past 6 years. Yet while it obsesses about a trivial miss that can not be meaningful in the context of an open economy, it fails to note that actual main street inflation—led by the four horseman of food, energy, medical and housing—–has been running at 3.1% per annum since the turn of the century.

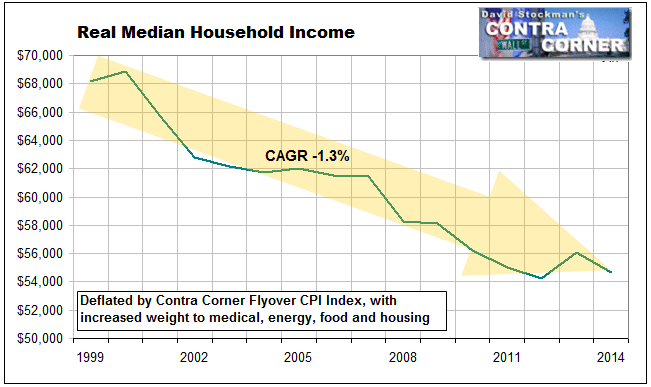

After 16 years this considerable annual gap, of course, has ballooned into a chasm. As shown in the graph, the consumer price level faced by flyover America is now actually 35% higher than what the Fed’s yardstick holds to be the case.

Stated differently, main street households are not whooping up the spending storm that our monetary central planners have ordained because they don’t have the loot. Their real purchasing power has been tapped out.

To be sure, real growth and prosperity stems from the supply-side ingredients of labor, enterprise, capital and production, not the hoary myth that consumer spending is the fount of wealth. Still, the Fed has been consistently and almost comically wrong in its GDP growth projections because the expected surge in wages and consumer spending hasn’t happened, causing it to double-down on the very policies that are generating the problem.

Even using the standard, understated CPI, real household income has been falling on an irregular basis since the turn of the century. That apparently does not phase the FOMC because their faulty model says they only thing that counts is spending—-even if from borrowed money and levered-up balance sheets.

Indeed, the Keynesian bathtub model is so primitive that households could be buried in twice today’s debilitating debt level—say $28 trillion versus the actual level of $14.2 trillion—and it would make no difference whatsoever. The more they borrowed, the higher would go the consumer spending and GDP computations.

In fact, however, real household income has plunged by 20% since the turn of the century when nominal incomes are deflated by our Flyover CPI. The chart-picture below actually explains better than the proverbial “thousand words” why the Fed is failing on the economic front and Donald Trump is succeeding in the political arena.

We will have more to say in future installments about how the Fed’s destructive policies are squeezing the purchasing power of main street wages and salaries, but in light of today’s release of more bad data on manufacturing shipments, which was falsely spun as positive news by the MSM, it is worthwhile to look at one of the key precursors of wage and salary income.

Needless to say, the rate of capital investment profoundly impacts the competitive position of flyover zone workers versus the rest of the world. Yet today’s release on April orders and shipments for core manufacturers CapEx (less defense and aircraft) not only documented that this so-called recovery is rolling over; it actually nailed our indictment of Fed policy to the wall.

As shown in the chart below, orders and shipments are now down nearly 12% and 10%, respectively, from their September 2014 cycle high. You can’t call double-digit declines evidence of escape velocity.

But here is the more startling thing. Manufactures’ CapEx today is no higher than it was in the spring of 1999!

Yes, $4 trillion worth of Fed money printing ago (when its balance sheet was less than $500 billion) the monthly rate of capital spending in nominal terms was higher than it is today. And in inflation-adjusted dollars, it has descended into the sub-basement.

Where has all the investment gone?

Funnily enough, Goldman Sachs explained it about as well as anyone. The share of corporate cash flow being pumped back into the casino in the form of stock buybacks and dividends is now at an all-time high of nearly 50%—-or nearly double its turn of the century level.

And even that understates the case because the overwhelming share of M&A deals are driven purely by financial engineering based on cheap debt and purchase accounting games with post-acquisition earnings. The truth is, upwards of 60% of projected S&P 500 cash flow for 2016 will be cycled back into Wall Street according to Goldman projections.

That’s about $1.3 trillion, and the reason is hardly subject to dispute. Fed policy has turned the C-suites of corporate America into stock trading rooms. Investments in flyover zone businesses which might pay-off 5 years from now can hardly compete with stock option winnings next quarter.

Indeed, Fed policy has had a double whammy effect on the flyover zone economy. It drove inflation up when down was needed; and its strip-mined capital from American business when increased capital investment was of the essence.

Despite all the Fed’s palaver about “low-flation” and undershooting its phony 2% target, American workers have had to push their nominal wages higher and higher just to keep up with the cost of living.

But in a free trade economy the Fed’s wage-price inflation treadmill was catastrophic. It drove a wider and wider wedge between US wage rates and the marginal source of goods and services supply in the global economy.

Accordingly, at the end of the day it was the Fed which hollowed out the American economy. Without the massive and continuous inflation it injected into the US economy, nominal wages would have been far lower, and on the margin far more competitive with the off-shore.

That’s because there is a significant cost per labor hour premium for off-shoring. The 12,000 mile supply pipeline gives rise to heavy transportation charges, logistics control and complexity, increased inventory carry in the supply chain, quality control and reputation protection expenses, lower average productivity per worker, product delivery and interruption risk and much more.

In a sound money economy of falling nominal wages and even more rapidly falling consumer prices, American workers would have had a fighting chance to remain competitive, given this significant off-shoring premium. But the demand-side Keynesians running policy at the Fed didn’t even notice that their wage and price inflation policy functioned to override the off-shoring premium, and to thereby send American production and jobs fleeing abroad.

Needless to say, that giant blunder has gut-punched flyover America at its most vulnerable spot. That is, among workers with less than a college education.

And contrary to establishment propaganda, the devastating decline in the employment/population ratio shown below is not due to an aging demographic. The over 65 population’s workforce participation rate has actually soared.

The latter trend probably explains where Wal-Mart finds its greeters.

But both lines on the chart surely point to where the Donald is finding his voters.

No comments:

Post a Comment