by David Stockman

In the case of America’s 80 million working age adults (25 or over) with a high school education or less, the Fed’s double whammy has been catastrophic. As we demonstrated yesterday, the employment-to-population ratio for this group has plummeted from 60% prior to the great recession to about 54% today.

In round terms this means that the number of job holders in that pool of the less educated has shrunk from 49.4 million to 43.5 million since early 2007. That’s nearly 6 million workers gone missing or 12% of the total from just nine years ago.

And as we documented yesterday this plunge is not due to aging demographics. The MSM meme that it’s all about the baby boomers hanging up their spikes doesn’t wash; the labor force participation rate of persons over 65 has actually increased sharply in recent years.

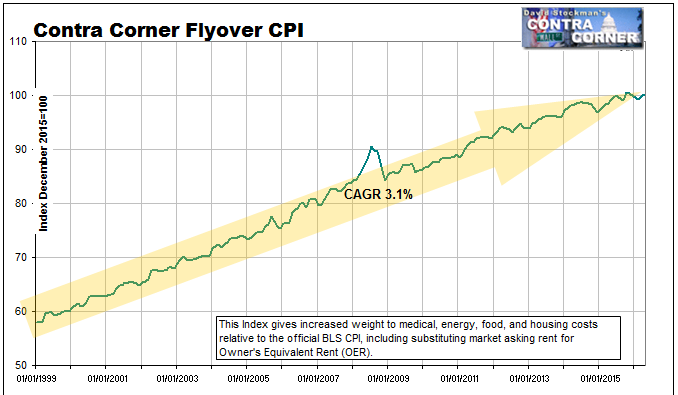

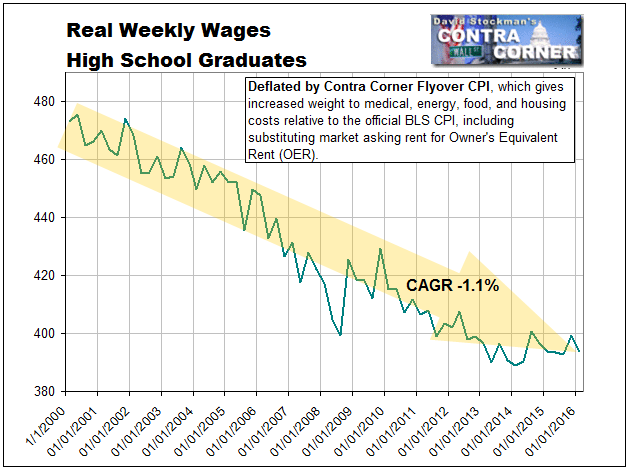

But even those who have managed to stay employed have suffered a devastating reduction in purchasing power. In fact, based on our Flyover CPI, each dollar of wages would buy 3.1% less annually or a cumulative 70% less since 1999.

And that assumes just 65% of the budgets of these lower-wage households are consumed by the four horsemen of inflation—-food, energy, medical and housing. There can be little doubt that they actually spend a materially greater share on these necessities than we have allocated to them in our index.

By contrast, nominal wages rates for the high school and under workers have risen by less than 50% over the same period. That means drastic purchasing power compression.

In fact, flyover America’s vast cohort of less educated workers has experienced an approximate 1.1% decline in their real weekly wages every year this century. In 2015 dollars of purchasing power, average pay has declined from $475 per week to $397 per week.

That’s right. When viewed on an annualized basis, households which were scrapping by on $24,700 per year in 2000 have seen the purchasing power of their pay checks drop to $20,600 today or by nearly 17%.

Yet the house of academic fools in the Eccles Building keep insisting that we have insufficient inflation!

Likewise, the all knowing pundits of the Acela Corridor (Washington/Wall Street) can’t figure out why Donald Trump has come roaring out of nowhere.

That gets us to the Wall Street/Keynesian cult of consumer spending. The latter holds that Americans who “shop until they drop” are the mainspring of the US economy based on the silly observation that personal consumption expenditures (PCE) comprise 70% of the GDP accounts, which themselves are a Keynesian construct.

Then again, no one told them that fully $3.5 trillion or 28% of total PCE consists of imputed housing consumption via OER (owners equivalent rent) and health care costs heavily funded by third-parties such as government entitlements and employer-based health insurance plans. No one “shopped” to fund either of these huge PCE components, but self evidently someone worked to pay the taxes and premiums.

That is, real capitalist growth and prosperity stems from the supply-side ingredients of labor, enterprise, capital and production, not the hoary myth that consumer spending is the fount of wealth.

Yet even within the framework of our Keynesian monetary central planners, how did real PCE grow so strongly during the last two decades when real incomes for a huge share of the work force were falling so sharply?

In a word, debt. The flip-side of the Greenspan/Bernanke/Yellen wage crushing operation was a national LBO in the household sector.

During the 21 years between Greenspan’s arrival at the Fed in August 1987 and the early 2008 peak, household debt erupted from $2.7 trillion to $14.3 trillion or by 5.3X.

To be sure, nearly $12 trillion of extra debt, representing an annual growth rate of nearly 8.5%, speaks for itself in terms of the implied monumental excess. But our Keynesian witch doctors have a way of attempting to minimize the import of it by what we call the “inflation lockstep fallacy”.

That is to say, there is purportedly not so much to see here because much of this huge gain represents inflation; and, of course, wages and incomes were inflating over this 21 year period, too. What counts, or so claim our Keynesian bettors, is “real dollar” amounts as computed by their bulimic inflation indices.

Au contraire!

Wages in the Chinese export factories were not being set by the PCE deflator less food and energy as confected and tabulated by some GS-16s in the BLS’ statistical puzzle palace. On the margin, the “China price” in the world’s labor market was less than $1 per hour equivalent during most of that time.

And that’s a full stop. Constant dollar statistical deflators had nothing to do with it.

The Fed’s policy of systematically and massively inflating the domestic cost of living and household debt, therefore, resulted in a giant economic deformation—-one even greater than that implied by the parabolic debt gains through 2008 shown above.

Indeed, the full import can only be grasped by considering the sound money contrafactual case. To wit, as we demonstrated in an earlier post on this topic the CPI would have declined by 1-2% per year under a sound money regime after the early 1990’s when China’s export machine took off.

That means that even under a scenario of 3% labor productivity growth and constant household leverage ratios (i.e. debt-to income), total household debt would have grown by perhaps 2% per annum.

So by 2008 outstanding household debt would have been in the range of $4 trillion, not $14 trillion.

That’s right. Thanks to the utterly wrong-head monetary policies of Greenspan and his successors, US households ended up with $10 trillion of extra debt to lug around. And in the bargain, they got bloated nominal wage rates, which resulted in the massive off-shoring of their jobs, and shrinking purchasing power, which lowered the living standard of the less educated flyover zone work force by 17% just since the turn of the century.

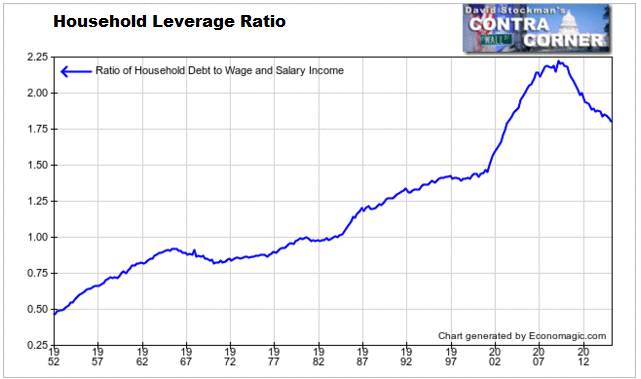

The extent of this destructive household sector LBO is hinted at in the graph below. Historically, the ratio of household debt—-mortgages, credit cards, car loans and the rest—–was under 80% of wage and salary income.

After Nixon pulled the props out from the last vestiges of sound money at Camp David in August 1971 and turned the Fed loose to print at will, however, the ratio began to creep steadily higher.

Yet it was only after the arrival of Greenspan in the Eccles Building that the household leverage ratio went virtually parabolic, climbing from about 100% of wages and salaries to nearly 225% by the early 2008 peak.

We have called this a one-time parlor trick of monetary policy because while the leverage ratio was rising, it did permit households to supplement spending from their current wages and salaries with the proceeds of incremental borrowings. Undoubtedly, this artificial goosing of living standards by the central bank money printers did help insulate flyover America from feeling the full brunt of its shrinking job opportunities and the deflating purchasing power of its pay checks.

No more. The household LBO is over and done, but the slightly declining leverage ratio shown in the chart is not a measure of progress; it’s an indicator of the distress being felt by households that have been forced to cut their consumption expenditures to the level of current earnings, which, in turn, are not rising nearly as fast as the 3.1% inflation rate afflicting flyover America.

There is no secret or mystery as to how America’s working households were led into this appalling debt trap. The fact is, the befuddled Greenspan actually bragged about it when he celebrated the higher consumption levels that were being funded by MEW or mortgage equity withdrawal.

That was just Fedspeak for the fact that under its interest rate repression policies, American families were being massively incentivized and encouraged day and night by cash-out mortgage financing ads ( e.g “Lost another one to Ditech!”) to hock their homes to the mortgage man and splurge on the proceeds. This reached nearly a $1 trillion annual rate and 9% of disposable personal income at the peak just before 2008.

That Greenspan took great pains to track the data and publish the above chart is a measure of how far the Fed had descended into “something for nothing” economics.

Did they think that the leverage ratchet would never stop rising? Did they not recognized the fundamental economic fact of the present era? Namely, that there is a massive 80-million strong baby-boom generation heading for retirement and that for better or worse, home equity accumulation owing to the deductibility of interest has been its primary vehicle of savings?

Well, apparently not in the slightest. Here is what was happening behind the screen during Greenspan’s spurious MEW campaign. American households were strip-mining the equity from their homes and burying themselves in mortgage debt.

Total mortgage debt outstanding soared from $1.8 trillion to $10.7 trillion or by nearly 6X during this 21 year period. And even though housing prices more than doubled, the ratio of equity to owner-occupied housing asset value plunged from 67% to 37% over the period.

Here’s the thing. The MEW party ended nine years ago, but virtually all of Greenspan’s MEW is still there. Flyover America may not know exactly how it got buried in such massive debts, but it knows that the current Washington/Wall Street Bubble Finance regime has left it high and dry. It now suffers a relentless shrinkage of living standards even as these contractual debt obligations chase the huge cohort of baby-boomers right into their retirement golden years.

The only thing worse than the MEW legacy plaguing seniors is what’s happening on the other end of the demographic curve. Among student age Americans, the degree of debt enslavement has become even more draconian.

In the last decade alone, total student loans outstanding have nearly tripled, rising from $500 billion in 2006 to $1.34 trillion at present. And for reasons laid out below, a disproportionate brunt of this massive student loan burden is being shouldered by flyover America.

That’s mainly because the preponderant share of the nation’s 25 million higher education students comes from the flyover zones. Those precincts still had a semblance of a birth rate 25 years ago, unlike the culturally advanced households of the bicoastal meccas.

Stated differently, these staggering debt obligations were not incurred by Wellesley College art history majors or even needs-based diversity students at Harvard Law School. They are owed by the inhabitants of mom and pop’s basements scattered over the less advantaged expanse of the land.

After all, the Ivy league schools including all of their graduate departments account for only 140,000 students or 0.5% of the nation’s total. Even if you add in the likes of MIT, Stanford, Caltech, Northwestern, Duke, Vanderbilt and the rest of the top 20 universities you get less than 250,000 or 1% of the student population.

The other 24 million are victims of the feckless Washington/Wall Street ideology of debt and finance. To wit, tuition, fees, room and board and other living expanses have erupted skyward over the last two decades because Washington has poured in loans and grants with reckless abandon and Wall Street has fueled the madcap expansion of for-profit tuition mills.

Even setting aside the minimum $50,000 annual price tag at private institutions, the tab has soared to $20,000 annually at public 4-year schools and nearly $30,000 per year at the tuition mills.

These figures represent semi-criminal rip-offs. They were enabled by the preternaturally bloated levels of debt and finance showered upon the student population by the denizens of the Acela Corridor.

So the former now tread water in an economic doom loop. Average earnings for 35 year-olds with a bachelors degree or higher are $50,000 annually, compared to $30,000 for high school graduates and $24,000 for dropouts.

Thus, the sons and daughters of the flyover zones feel compelled to strap-on a heavy vest of debt in order to finance the insanely bloated costs of higher education. But once so “educated”, the overwhelming majority end up with $30,000 to $100,000 or debt or more.

In this regard, the so-called for-profit colleges like Phoenix University, Strayer Education and dozens of imitators deserve a special place in the halls of higher education infamy. At their peak a few years ago, enrollments at these schools totaled 3.5 million.

But overwhelmingly, these “students” were recruited by tuition harvesting machines that make the all-volunteer US Army look like a piker in comparison. To wit, typically 90% of the revenues of these colleges were derived from student grants and especially loans——-hundreds of billions of them—-but less than one-third of that money went to the cost of education, including teachers, classrooms, books and other instructional costs.

At the same time, well more 33% went to SG&A and the overwhelming share of that was in the “S” part. That is, prodigious expenditures for salesmen, recruiters, commissions and giant bonuses and other incentives and perks.

Needless to say, this made for good growth and margin metrics that could be hyped in the stock market. In fact, after the cost of education and all of the massive selling expense to turbocharge enrollment growth was absorbed, there was still upwards of 35-40% of revenue left for operating profits.

That’s right. For a decade until the Obama Administration finally lowered the boom after 2011, the fastest growing and most profitable companies in America were the for-profit colleges.

In short order they became a hedge fund hotel, meaning that the fast money piled into the for-profit college space like there was no tomorrow. So doing, they often drove PE ratios to 60X or higher, bringing instant riches to start-up entrepreneurs and top company executives, who, in turn, were motivated to drive their growth and profit “metrics” even harder.

At length, they became tuition mills and Wall Street speculations that were incidentally in the higher education business, or not. The combined market cap of the six largest public companies went from less than $2 billion to upwards of $30 billion in a decade.

The poster boy for this scam is surely Strayer Education. Between 2002 and the 2011 peak, its sales and net income grew at 25% per year and operating profit margins clocked in at nearly 40%.

Not surprisingly, Strayer was peddled as the second coming of “growth” among the hedge funds. The momo chasers thus pushed its PE ratio into the 60-70X range in its initial growth phase, and it remained in the 30-40X range thereafter.

Accordingly, its market cap soared by 7X from $500 million to $3.5 billion at the peak. The hedge funds made a killing.

STRA Market Cap data by YCharts

Then the Federal regulators threw on the brakes, and it was all over except the shouting. Total market cap of more than $27 billion disappeared from the segment within three years after 2011 and the hedge fund hotel experienced a mass stampede for the exits.What was left were millions of flyover zone thirty-something’s stuck with crushing unpaid loans, educations of dubious value and a lot more years in mom and pop’s basement.

Should any of these tuition mills have even existed, let alone been valued at 60X earnings——-earnings that did not derive from real economic value added and which were totally at the whims of the US department of education?

Of course not.

But then again, after 20 years of radical financial repression the Wall Street has been turned into a casino that scalps the flyover zone whenever it gets half the chance.

No comments:

Post a Comment